A Smarter Way to Think About Retirement Income

This is a follow-up to my earlier post, "Rethinking Monte Carlo Simulations," in which I argued that the standard "probability of success" framing leaves retirees anxious and with few actionable answers. If you haven't read it, the short version is this: retirement isn't pass/fail, and a good plan shouldn't treat it that way.

That post ended with a teaser about the dynamic guardrails approach — a framework that actually answers the two questions retirees care most about:

How much can I spend each month?

When would I need to adjust, and by how much?

This post is the follow-up.

The 4% Rule: A Good Starting Point, But a Rigid One

For decades, the 4% rule has been the default answer to "how much can I safely spend in retirement?" It comes from a 1994 study by financial planner Bill Bengen, later reinforced by the so-called Trinity Study out of Trinity University. The research examined historical market returns dating back to 1926 and asked: What's the highest withdrawal rate that would have survived every 30-year retirement period in the historical record, including the worst periods?

The answer was roughly 4%. Withdraw 4% of your portfolio in year one, adjust that dollar amount for inflation each year, and history suggests your money should last at least 30 years.

That was a genuinely useful insight. Before Bengen's work, retirees had little more than intuition and rules of thumb to guide their spending. Having a research-backed starting point was meaningful progress.

The problem is that the 4% rule is static. Once you set your withdrawal amount, it doesn't change — not when the market drops 30%, not when you turn 80, not when your spending needs shift. It's a straight line drawn across what is, in reality, a complicated and changing landscape. For most retirees, that rigidity leads to unnecessary deprivation — spending less than they could have, well into their eighties, with far more left in the bank than they'll ever need. For others, it could mean spending confidently in a deteriorating situation, with no clear signal for when to pull back.

A good retirement income plan should do better than that.

A Better Approach: Dynamic, Risk-Based Guardrails

The guardrails framework — pioneered in its early form by researchers Jonathan Guyton and William Klinger in 2006 — introduced a more adaptive concept: rather than locking in a fixed spending level at retirement and holding it forever, you establish a spending level along with clear thresholds for when to adjust up or down based on what's actually happening with your portfolio.

We use a more sophisticated version of this idea, one that goes well beyond tracking withdrawal rates. Instead of a simple rule tied to a single metric, it accounts for the full complexity of a real retirement:

Upcoming income sources. Most retirees don't draw exclusively from their portfolio for their entire retirement. Social Security typically begins a few years in. A pension might start on a different schedule. A property might be sold. A static withdrawal model treats these events as outside the plan; a risk-based approach builds them in from day one and adjusts spending capacity accordingly.

Age and time horizon. A 62-year-old with $2 million faces very different risks than a 78-year-old with the same balance. As you age, your planning horizon shortens, which generally means you can sustainably spend more from the same portfolio. A good model reflects this reality and updates continuously.

Inflation and market conditions. Rather than applying a blanket inflation adjustment regardless of circumstances, the approach incorporates current conditions—how the portfolio has performed, how inflation has eroded purchasing power, and the outlook going forward.

Changing spending needs over time. Research on actual retiree spending patterns consistently shows that spending tends to be highest in the early, active years of retirement, gradually declines through the middle years, and then often increases again in the final years — primarily due to healthcare and care costs. This pattern is sometimes called the "retirement smile." A static model ignores this shape entirely. A dynamic approach can reflect it, allowing higher spending in the early years when clients are most likely to benefit, and incorporating realistic assumptions for later years when care costs tend to rise.

Long-term care costs. This is one of the most significant and most often underplanned financial risks in retirement. Rather than leaving it as an open question, we build an estimate of potential care costs into the plan from the start by assuming higher expenditures in later years. This isn't a one-size-fits-all number — we refine those assumptions for each client based on their insurance policies, health history, family situation, and preferences.

The guardrails themselves are expressed in dollars, not percentages. Rather than telling a client, "Your withdrawal rate has crossed a threshold," we can say, "If your portfolio falls to $X, we'd recommend reducing spending by $Y." That's an answer you can actually do something with.

We use a software platform called Income Lab to build, monitor, and update these plans, running the analysis continuously so we always have a current view of where the plan stands and whether any adjustments are warranted.

What This Looks Like in Practice

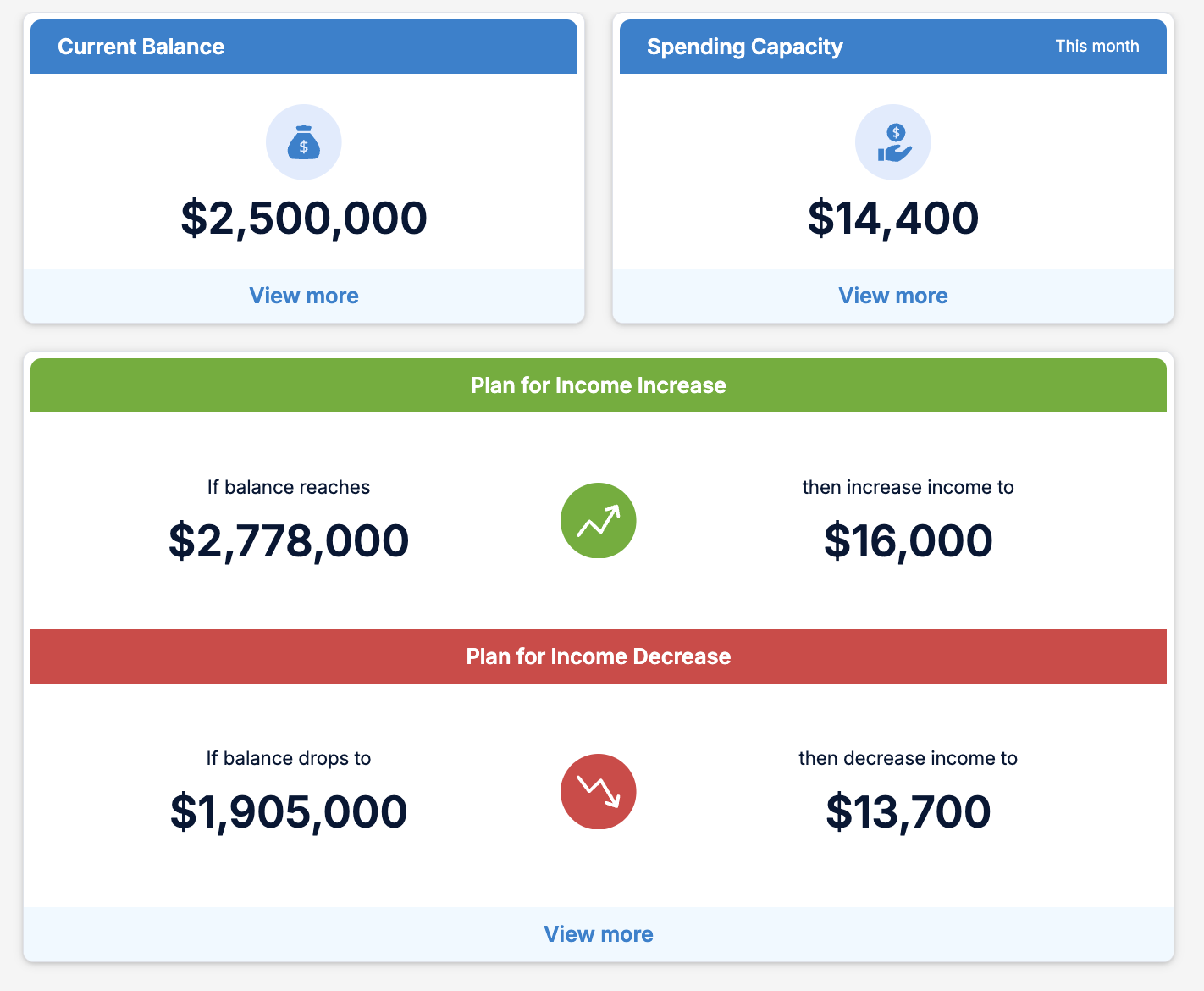

Consider a couple — let's call them the Petersons — who retire at 62 and 60, with a combined $2.5 million investment portfolio. Social Security is scheduled to begin at age 67 for one spouse and at 62 for the other. They have no pension.

Values shown in today's dollars and rounded. Income values are monthly and gross of tax, savings, and variable expenses.

Source: Income Lab

Their spending capacity reflects the monthly gross income they can sustainably spend, right now. The guardrails below show the portfolio balances where we'd increase spending and where we'd need to pull back. That's the plan.

Viewing retirement planning this way gives the Petersons clarity. Rather than a probability-of-success score that requires interpretation, they can see exactly where they stand.

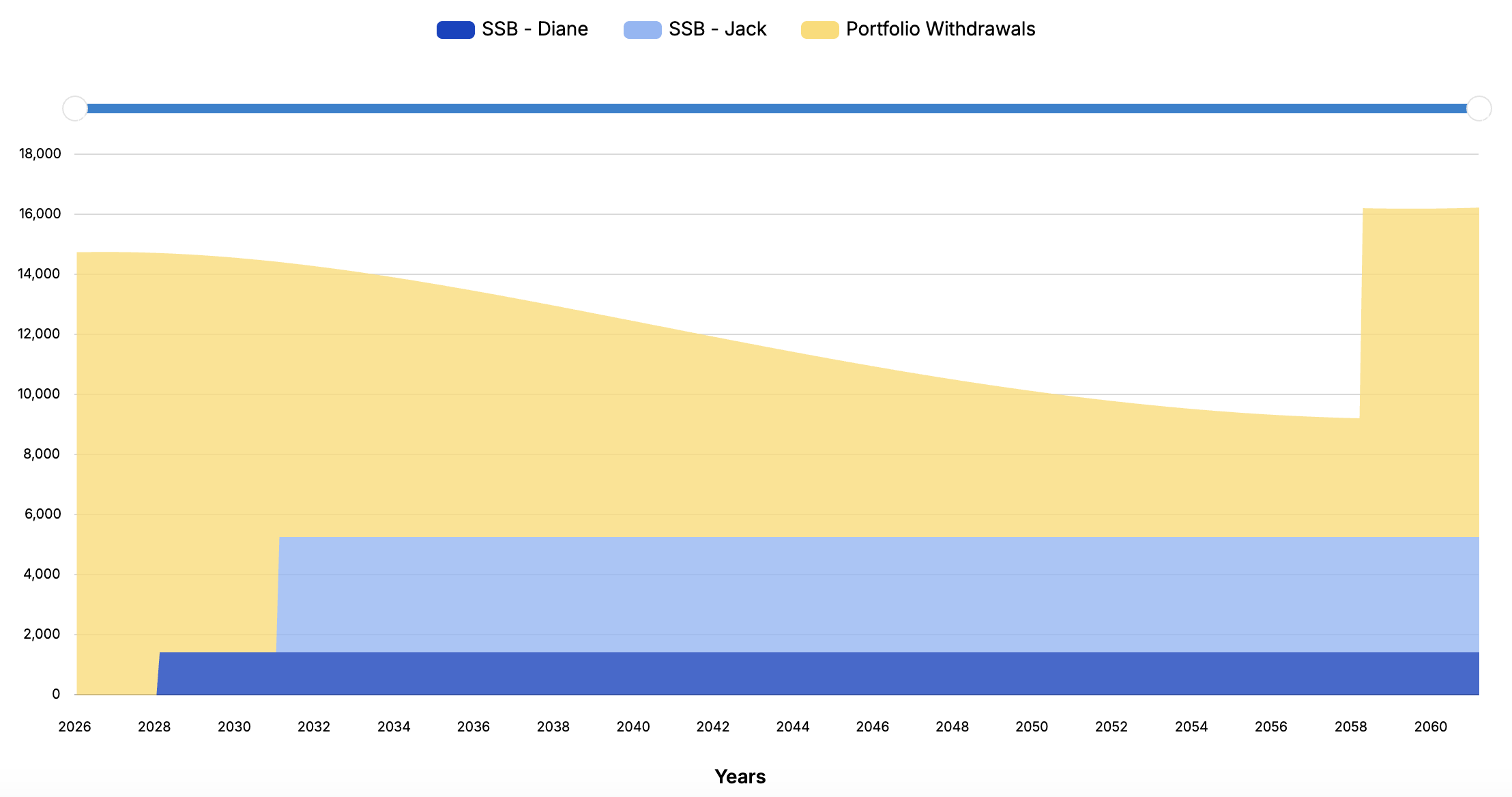

The next chart shows how the Peterson’s income sources change over time.

Income values are monthly and gross of tax, savings, and variable expenses.

Source: Income Lab

In the early years of retirement, the Petersons' portfolio is doing most of the heavy lifting. Withdrawals are at their highest. Under a static model, this can look alarming — withdrawal rates are elevated, and the portfolio is drawing down. But a risk-based approach recognizes that this picture changes significantly when Social Security begins, and portfolio withdrawals drop substantially. The plan was built with that transition in mind.

As the Petersons move through their seventies, the plan reflects the natural shift in spending patterns — somewhat less on travel and discretionary expenses, somewhat more on healthcare. And in the later years of the plan, care costs are already accounted for. Not as a worst-case scenario, but as a built-in assumption that can be revisited and refined as the picture becomes clearer.

A Plan You Can Trust

The goal was never a perfect plan. The future is too uncertain for that, and anyone who tells you otherwise is selling something. The goal is a plan with enough structure and clarity that you know when you're on track, when conditions warrant an adjustment, and what that adjustment should look like.

The dynamic guardrails approach gets much closer to that goal than a static withdrawal rule or a probability score ever could. It reflects the actual complexity of retirement — the income shifts, the spending changes, the uncertainties — and gives you a robust framework for navigating it.

In a future post, I'll walk through a more detailed scenario to show how this plays out over a full retirement timeline, including what an adjustment might actually look like when market conditions shift.