Articles by Oakleigh Wealth

A Smarter Way to Think About Retirement Income

The 4% rule gave retirees a research-backed starting point. But it's static — it doesn't care what the market is doing, how old you are, or whether your income picture has changed. Here's a better framework.

The Backdoor Roth IRA

Roth IRA accounts are one of the most tax efficient retirement savings vehicles. But if your income is over the phase-out limits, you will not be able to contribute directly to your Roth IRA. Enter the so-called “backdoor Roth,” a loophole which allows you to add to your Roth IRA when your income is otherwise over the limit. BUT… it doesn’t come without risk.

Should I take My Pension as a Lump Sum?

For many, employer pensions are a key part of retirement planning. While these plans are increasingly rare, they often represent a significant portion of anticipated retirement income. If you're nearing retirement or already receiving pension payments, you may face an important decision: Should you opt for a lump sum distribution or continue receiving a lifetime stream of payments?

Social Security Strategies

The majority of Americans depend on two main sources of retirement income: their investment portfolio and their social security benefits. It’s no wonder then that the financial stability of this popular and important program is politically sacrosanct or that it receives so much media attention. And yet, so many Americans, (particularly those who rely most on the benefits), don’t have a good framework for making the optimal claiming strategy.

The Three Retirement Tax Landmines

Navigating the financial landscape of retirement can be fraught with challenges, particularly when it comes to taxes. Among the most significant tax pitfalls that retirees must contend with are the "three tax landmines": Required Minimum Distributions (RMDs), the Widow's Penalty, and Beneficiary Taxes.

Why we wrestle with the shift from saving to spending

There are a couple of reasons why retirees might find it hard to switch from saving to spending:

Fear of running out:

Habit and mindset:

Loss of regular paycheck:

These anxieties are common, and there are strategies to contextualize and address them to develop a healthy spending plan in retirement. However, they also point to a universal human struggle that‘s observable from a young age: the difficulty balancing between present and future enjoyment.

Planning for long-term care in retirement

Insurance works best to cover risks that are both low in frequency and high in severity (car accidents, house fires, premature death, or disability). This is why LTC is so difficult to plan for: It’s not all that low in frequency, but it can also wreck your retirement plan. These two things conspire to make LTC much more expensive to insure against (whether that’s self-insuring or purchasing an insurance policy).

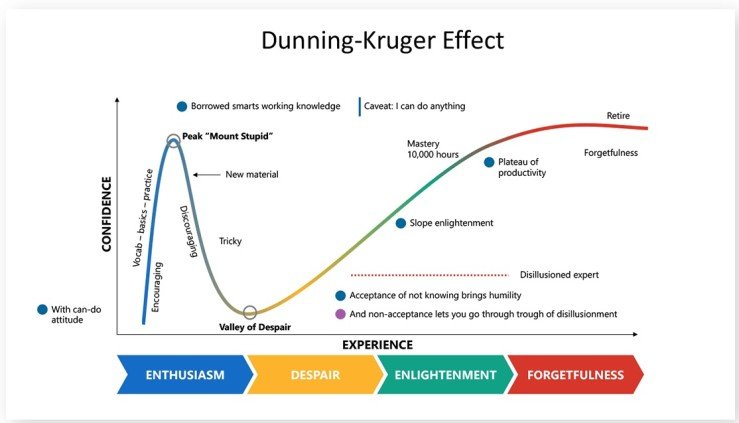

Retirement: Math Problem vs. Human Problem

I came across this fantastic illustration by British retirement podcaster and financial planner Dan Haylett a couple of weeks ago. It perfectly captures a dynamic I’ve written about on this blog more than a few times. Namely, the misperception we all have that financial planning is a math problem; an equation to be solved having either a right ora wrong answer.

Rethinking Monte Carlo Simulations

Monte Carlo simulations are a common tool in the financial adviser’s toolkit. They can help us frame the likelihood of success of a given plan by applying a large number of statistical simulations of future market returns to your financial plan.

On paper, this approach to financial planning makes a lot of sense; however, applying Monte Carlo analysis as an ongoing real-world decision-making tool often results in misunderstanding, anxiety, and/or overconfidence.

Look beyond bonds for sustainable retirement income

With the recent increase in interest rates, retirees or those nearing retirement might find it tempting to invest their nest eggs in longer-dated government bonds to secure a stable, long-term income. After enduring the "Great Financial Crisis," it's understandable why exiting the stock market might seem appealing. When you have only a few working years left or have already retired, the prospect of another market downturn can be quite daunting.

However, following this line of thinking could lead you into trouble!

Maximizing Your HSA’s Full Potential: Stop Using It Like an Expense Account

Health Savings Accounts (HSAs) allow you to pay for a wide variety of qualifying healthcare expenses with pre-tax dollars. But this may not be the best use of your HSA funds (at least not now).

If you have the financial means to pay your healthcare costs directly, you might find greater value in treating your HSA as a long-term retirement savings tool rather than a healthcare checking account. This is particularly advantageous if you are younger, in relatively good health, and can afford to pay for minor medical expenses out of pocket. In the long run, it may be in your best interest to invest those HSA dollars for the long term, allowing the balance to grow and compound tax-free for use later in life or in an emergency.

Defining the Elements

At Oakleigh, we use an app called Elements to show a quick snapshot of your financial health and track specific key metrics over time. This is very similar to how a doctor might track your vital signs to understand your physical health and quickly diagnose specific issues. Of course, there’s a story behind all of these numbers and we would dive much deeper for a full financial planning engagement. However, you might be surprised by how many important issues can be uncovered and addressed from these high-level metrics alone.

To Roth or Not to Roth? Deciding Between Roth and Tax-Deferred Savings

The decision of whether to contribute to a Roth or a traditional retirement account basically boils down to timing: do I pay taxes now or later? While both types of retirement accounts are powerful tools for building wealth, this seemingly simple binary can produce some unique planning opportunities with meaningful tax savings for many individuals.

Financial Assessment for a Couple In their Mid-30s

Ever wondered what a financial assessment looks like? Here’s an example assessment of a married couple in their mid-30s with two young children. Mike is an architect working for a larger firm making $95k per year and his wife Mary just received a raise at the consulting firm she works for, and is now making $260k per year after finishing an executive MBA program. They have two children in daycare, but they feel like they should be able to do more with the good money they’re making now, but life just continues to get more complicated.

How much should I be saving? Am I on track?

Your savings rate tells an important story about your current financial wellness and preparation for long term financial security. Setting a reasonable savings goal and sticking with it is highly correlated with financial independence. In this article, we'll answer following questions: How much should I be saving? Am I on track? How can I increase my savings rate?

Making Work Optional

This seemingly complicated question can be boiled down to a simple, but powerful metric: your Total term score.

This single number estimates the number of years a person could live on his or her current assets if they did not grow. This includes your cash, investments, business value, and real estate equity. While this key metric is not terribly difficult to calculate, it is powerful in its simplicity and its nuances can lead to very interesting discussions.

When can I afford to Retire? Part 3: Expenses

Making the transition from building your savings to spending it down can be a jarring one, but arming yourself with knowledge about your actual expenses can give you the confidence to make the transition, which may even be feasible sooner than you think.

Can I Afford to Retire? Part 2: Income

Once you’ve given some thought to what your ideal retirement looks like (see part 1), answering the question “When can I afford to retire?” becomes an exercise in comparing expected future expenses with expected future income over the rest of your life and your spouse’s life. In this second part, we’ll look at the income side of the equation and ask, “where is the money going to come from?”

Can I Afford to Retire (and when)?

“When can I afford to retire?” is the question that drives more individuals into the office of a financial planner than any other. The sooner you start asking it, the better. Too often, the more tangible and immediate concerns of career and family life enable us to put off thinking about retirement, except in the abstract. It seems so far off in the future that it can be difficult to wrap your head around, (that is, until it’s right around the corner!).

In part one of this three-part series, we’ll take a step back and question what will retirement mean for me?

Retirement Savings Waterfall

With so many different types of savings and investment accounts available, it can be hard to know where to put the money you’re diligently saving. This savings waterfall will help you capture various tax incentives, which when compounded over many years, can add up to make a significant difference. The basic idea is that you fill up each bucket before going to the next, and if the bucket doesn’t apply to you, move on to the next.