Can I make a “Mega Backdoor Roth” Contribution?

Say you have maxed out your IRA and 401(k) contributions and you still have the ability to save more. In certain cases, you may be eligible to make a Mega Backdoor Roth contribution, no matter your income level.

The strategy involves making a non-Roth, after-tax contribution to your 401(k) and then immediately

A. making an in-service distribution of those after-tax funds into your Roth IRA (via a direct, tax-free rollover) or

B. doing an in-plan Roth conversion (moving the after-tax contribution to your Roth 401k.

Under the right circumstances (and if your plan allows it), you may be able to contribute tens of thousands of dollars to a Roth IRA, even if you’re over the income threshold to make regular Roth IRA contributions.

However, the rules are very restrictive and prohibitive for most folks, and they can be difficult to navigate.

If your employer's retirement plan does not permit this strategy, consider making a regular backdoor Roth contribution.

Costly mistakes to avoid when using the "mega-backdoor” strategy:

Missing the match: Contributing too much on an after-tax basis that you miss out on some of the employer matches. Getting money into your Roth is great, but getting “free” money in the form of a match is always better.

Some plans suspend 401(k) contributions after an in-service distribution This means you’re missing out on being able to contribute to your 401(k) and get the employer match for some period of time (typically 90 days).

Double paying taxes. The 1099-R that you’ll receive after the in-service distribution may not have the correct information, or may not have all the information you need to account for this properly on your taxes. Box 1 will show the amount of the distribution, and Box 2a will show the amount that’s taxable (which should be zero, or else should equal only the gains, not the after-tax contribution itself). Often the administrator will leave Box 2a blank and check “Taxable amount not determined” in Box 2b, meaning it’s up to the individual to determine and report the taxable amount. This is often missed, resulting in your after-tax contribution getting taxed twice, ouch! Even tax professionals get this wrong, either because they don’t ask the right questions or don’t have the full picture, and then assume that it’s all taxable to avoid under-reporting.

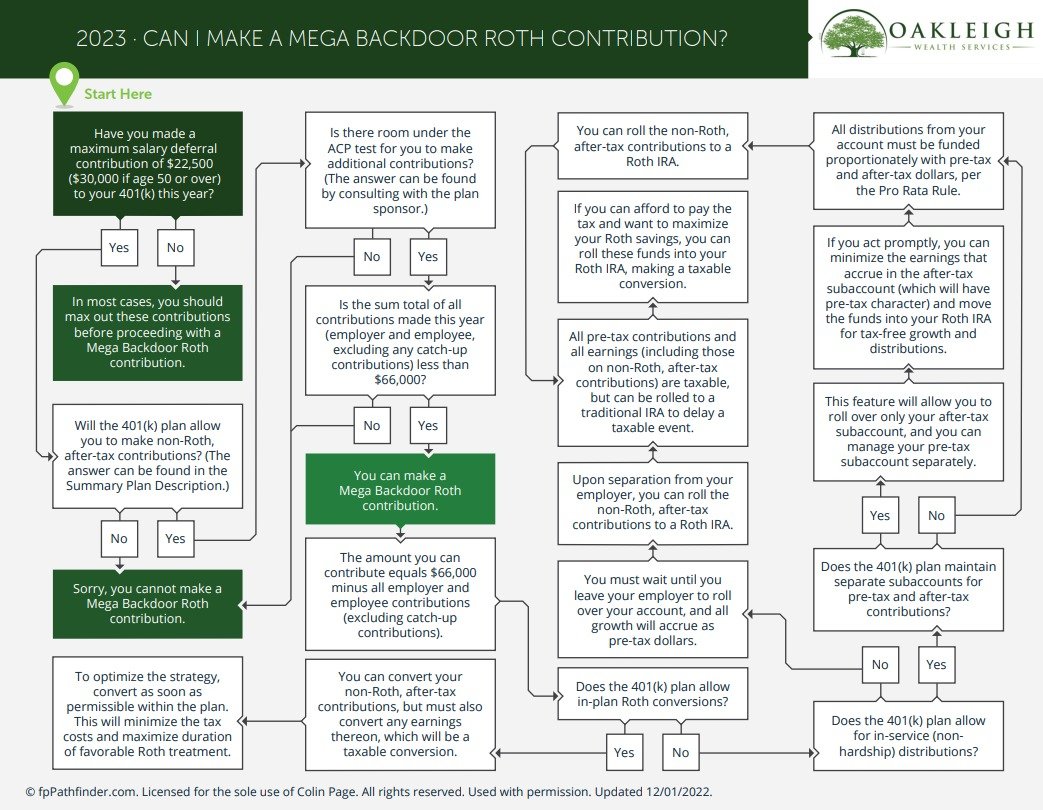

Can I make a Mega Backdoor Roth Contribution?

To help make the analysis easier, we use the “Can I Make A Mega Backdoor Roth Contribution?” flowchart. It addresses some of the most common issues that arise for a client trying to make a Mega Backdoor Roth contribution.

This flowchart considers:

The maximum amount that can be contributed

The impact of the ACP test

401(k) plan-specific features providing in-service distributions and/or separate accounts

The tax impact upon rollover

The step-by-step process to complete this kind of contribution

Before attempting this strategy, please consult your tax adviser and 401(k) plan documents to be sure you understand the steps and nuances involved. You may also need to reach out to the 401k administrator to execute certain steps or get clarity on what’s allowed.

It may be a good idea to reach out to a financial planner to talk about how the mega backdoor strategy fits into your comprehensive financial plan.

Click to download a pdf version!